PSF: 06_04_2026

Por: Eduardo Vanin

Artigo, Grãos

Publicado em: 04/12/2024 08:56

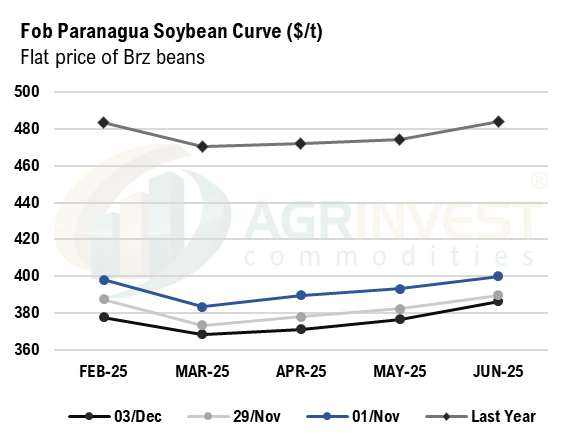

More producers in the center-west talking about the excessive rains, lack of sunlight and increasing diseases – higher cost. Farmer selling in Brazil remains subdue, for beans and corn. Many fear that the Brz real weakness is just the begging of a major downward spiral. Soybean crop size is big, no real threats for December and basis contnue to slid – no support from demand either. March traded at +0sh and May at +10sk – LW trades at +35sh and +47sk. Very few trades out of the US this week is not helping either. Sino booked only 3 cargoes for March so far – 13 Last week. Indications CFR China yesterday afternoon dropped more than 10 cents comparing to overnight. Seems tradings are liquidating longs. The China´s coverage for NC is about 6 Mi tons larger than LY. Inputs purchases in Brz is advancing ahead of LY. For safrinha 2025 the pace reached 70% (seeds, ferts and chemicals). For soybean 2025-26 the purchases are concentrated in potash. MAP is still much above of the historical ratio. Smeal sales in China this week is 551,800 tons, very similar to last week rhythm.